In our first co-authored post, we investigate the implications of Tax Breaks for businesses following the announcements of Chancellor of /Exchequer – Jeremy Hunt.

The rise in Corporation Tax for companies that pass a certain threshold had been in the country’s agenda for some time. And, it was met with a sceptical response upon its announcement by then-Chancellor Rishi Sunak in his budget of March 2021, scrapped by then-Chancellor Kwasi Kwarteng in his controversial mini-budget of September 2022, then brought back by Jeremy Hunt upon becoming Chancellor in October 2022.

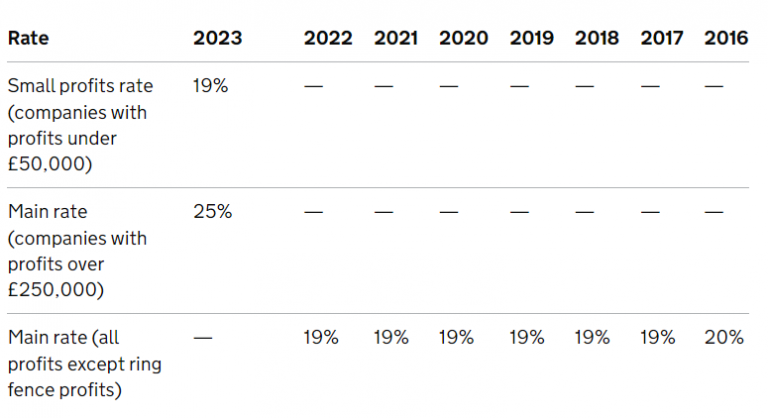

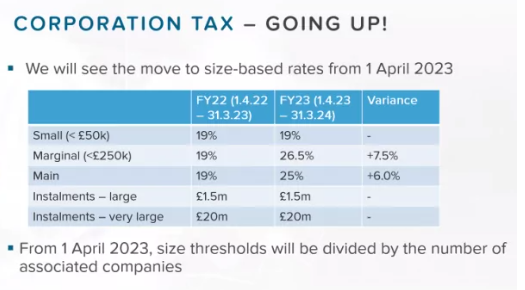

While the 19% rate has been the norm for the past six years for everyone involved, the new rates effective from April will impose a 25% Corporation Tax liability onto those with profits exceeding £250,000.

This development marks the first time since 1973 that the rate has been raised. In the 50 years since then, the rate gradually trickled down from 52% to 19%.

An important point to note here is that companies with profits between £50,000 – £250,000 will pay tax under a main rate but reduced by a marginal relief. This is described as a ‘gradual increase’ in the Corporation Tax rate between the small profits rate and the main rate.

Source: MCL Accountants

Anticipatedly, the adjustment in rates aims to address the gaps in the government’s finances resulting from the pandemic. However, this solution may lead to increased taxes on businesses, potentially hindering growth and reducing the appeal of investment opportunities in the UK. Various arguments have been made both in support of and against this assessment.

During Liz Truss’s brief interregnum, she and chancellor Kwasi Kwarteng argued that lower corporation tax rates would encourage investment in Britain and generate a yearly economic growth rate of 2.5%. Furthermore, the outlook of the country would be even more welcoming towards foreign investment:

In effect, it may then be beneficial to observe where Corporation Tax stands as a source of government revenue:

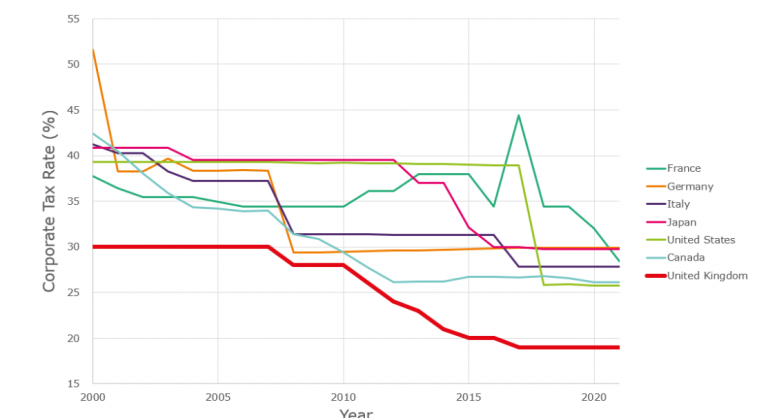

Furthermore, we can preface our argument with the fact that Corporation Tax is not exactly the highest ‘earner’, which only follows income tax, capital gains tax, NICs & apprenticeship levy (indicated in blue) and VAT (indicated in orange) in terms of the country’s overall tax take.

Another thing that stands out from the graph is that from 2001 to 2022, despite the main rate of Corporation Tax dropping from 30% to 19% over this period, it has remained roughly the same as a proportion of government revenue. The overall argument from PM Rishi Sunak’s end has been the comparatively low 10 per cent of companies that would effectively be liable towards the overall 6% hike.

To offset this rise, the Chancellor announced the initiation of a comprehensive and strategically targeted scheme designed to enhance the United Kingdom’s overall productivity and innovation capacity by incentivising investment in advanced technologies and research. This multifaceted plan encompasses tax relief measures and financial allowances for businesses investing in IT equipment, industrial plants, and machinery. With this ‘full capital expensing’ policy in place, a corporation tax cut of about £9 million is expected per year, adding that new economic policies are likely to lead to a visible increase in business invesment each year.

Under the purview of this sophisticated initiative, businesses will have the opportunity to deduct the entire amount spent on the aforementioned assets from their taxable profits. This policy aims to encourage enterprises to invest in the technological infrastructure necessary to bolster their operational efficiency and maintain competitiveness within the global market.

Furthermore, for small and medium-sized enterprises (SMEs), the Annual Investment Allowance (AIA) will experience a significant augmentation, with the threshold being elevated to £1 million. Consequently, this adjustment is projected to impact approximately 99 per cent of all businesses in the UK, enabling them to fully deduct the value of their capital investments from the taxable profits generated during that fiscal year.

In addition to the aforementioned provisions, the Chancellor’s announcement also includes supplementary tax support specifically tailored to assist research and development-intensive SMEs. This bespoke fiscal relief mechanism is designed to stimulate innovation and accelerate the commercialisation of cutting-edge technologies and discoveries.

Under the terms of this targeted tax relief scheme, eligible SMEs will be entitled to claim £27 for every £100 expended on qualifying research and development activities. This substantial financial incentive is expected to empower R&D-focused enterprises to allocate additional resources towards the pursuit of ground-breaking innovations, ultimately driving the nation’s economic growth and fostering a competitive advantage within the global marketplace.

Essentially, Britain is in need of higher productivity and capital investment where companies would have more funds to invest in capital or R&D, while the lower rate raises the profile of the UK as an investment destination.

Analyses also underline that while the UK economy has been recovering (sort of) from the effects of the COVID-19 pandemic and the markets have responded positively to Rishi Sunak’s arrival in Downing Street, labour market participation remains a structural problem. The UK’s workforce has been rising since over the last decade despite the ageing population but is currently 520,000 people fewer than the forecasts of the Office for Budget Responsibility (OBR).

The European Economic Policy Committee lists the antidote to labour participation as a dependancy on ‘enhancing employment opportunities by fostering both the demand and supply for labour’. Therefore, efficient product and services markets under favourable macroeconomic conditions are critical for both boosts in employment and participation to the labour force.

Bearing in mind that most newly-launched businesses and start-ups will still benefit from the 19% Corporation Tax rate, Britain needs all the help it can get from a wider pool that does not strictly rely on the domestic talent.

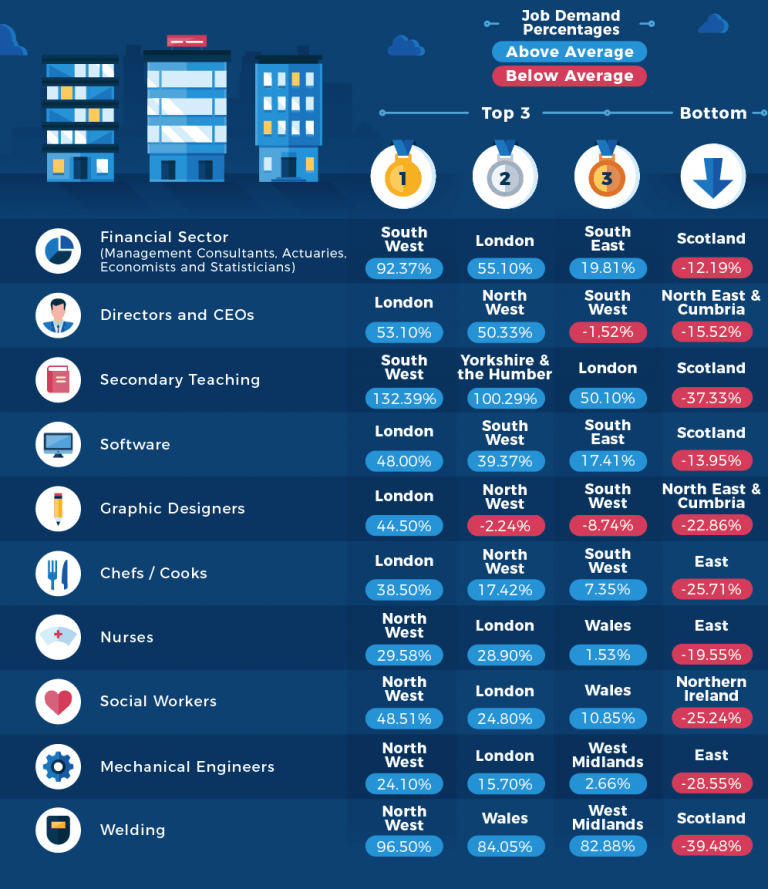

In fact, a recent YouGov poll revealed that close to half of Britons thought there was too much immigration, against a majority that wanted more foreign doctors, care workers, farmers, builders, and waiters in the workforce. These needs can further be corroborated from the Government’s perspective where the need for certain occupation groups is still prevalent:

The spring budget seems to have struck a delicate balance between fiscal responsibility and supporting growth. With a sprinkle of tax relief here, a dollop of investment there, and a generous helping of infrastructural improvement, Jeremy Hunt’s budgetary recipe will hopefully satisfy the taste buds of the UK’s economic as well as workforce palate.

While no one expects the British economy to turn into a turbo-charged, rocket-propelled juggernaut overnight, the Chancellor’s optimism has brought a refreshing sense of hope to the dreary post-Brexit landscape. Indeed, the UK appears to be shedding its cocoon of uncertainty and is poised to flutter toward a brighter economic future – just in time for the summer season.

Of course, as with any economic plan, there’s always the potential for a few unexpected bumps in the road – or, in the case of the UK, perhaps more potholes than we’d care to admit. However, we must hope that this will begin a promising new chapter in UK’s history and that it ushers in an era of prosperity, innovation, and a future where the only thing more reliable than the UK’s business environment is its bad weather.

Should you need guidance pertaining to your Individual, Business or Humanitarian UK immigration matter,

To arrange meeting with our lawyers, contact us by telephone at

+44 2077202156 or by email at office@goodadviceuk.com.

If you have instructed us before, we would be pleased to know your feedback about your experience.

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |